This dimension of the AI index addresses AI-related industrial activity.

It aims to reveal how AI is approached by private economic players worldwide and in the EU Member States, especially with respect of the development of core-businesses in AI, i.e., the creation of companies with a main activity in AI, and the involvement in the filing of AI-related patent applications.

In this sense, the objective is to understand how many enterprises are already focusing their businesses on AI (e.g., trading AI-based services), and how many of them are developing AI as support for their non-AI main economic activity (e.g. in the automotive sector).

In addition, a focus on robotics is proposed as its connections with AI are very likely to be even tighter in the near future. Indeed, the combination of AI and Robotics is starting to produce a new set of products and tools that are even more capable of interacting with the physical reality than the current generation of AI-based devices.

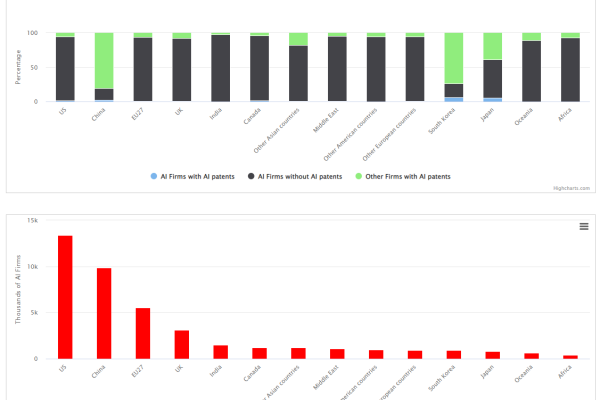

The US is home to the highest number of AI firms worldwide (more than 13,000), followed by China (almost 10,000), the EU (more than 5,500) and the UK (more than 3,000). Thus the EU appears to have a secondary role after the US and China. However, the size and productivity of the firms are aspects that are not considered in this analysis, and additional information in this regard may reveal a different picture. Here, again, the impact of Brexit can be noticed, with the UK accounting for approximately 40% of the AI firms previously part of the EU28 landscape.

When considering the top geographic areas (the US, China, the EU and the UK), it is possible to observe a very different profile for China compared with the others. Indeed, most of its firms are engaged in patenting activity (which is not the case for the US, the EU and the UK). This strong focus of Chinese industry in patenting is due to a different approach to this type of intellectual property. The reference is to lower standards of quality[1], which, on the one hand, ultimately induces more applicants to present a filing, and on the other hand, it also reveals the modest innovative potential of these patents.. In addition, in recent years, a series of governmental subsidies related to the development of patents has attracted a multitude of firms to patenting activity, and the number of filed patents has increased substantially. These elements therefore suggest that the observed patenting activity in China does not fully correspond to its true innovative capacity.

We identify three types of AI firms: those with a core business in AI that do not patent, those that only file AI-related patent applications, and those with a core business in AI and filing patent applications. The latter usually correspond to high-tech companies, and the largest number of those are located in the US and China (233 and 226, respectively, corresponding to 1.7% and 2.2% of AI firms in those countries). This insight confirms the leading position of these two countries in this domain. In this respect, the position of the EU is more modest, since just 43 firms (0.7% of all EU AI firms) have a core business in AI and file AI-related patent applications.

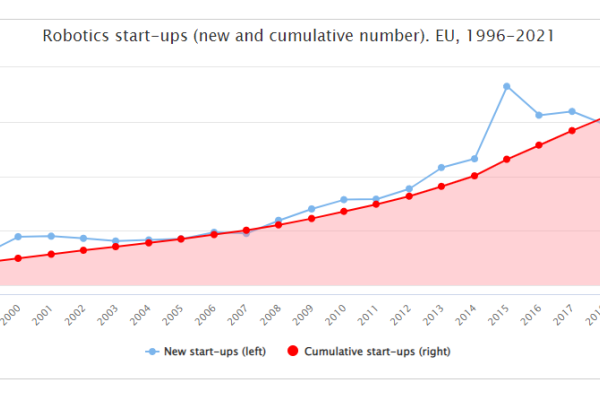

Important signals for the EU are found in the robotics sector. The analysis of the number of start-ups over time shows that in the EU this sector has been able to consistently attract entrepreneurs to found new firms. Since the late 1990s 4,000 new enterprises have been founded, with an upward trend of newly created start-ups until 2015, since when it remains relatively constant (at a level of around 300 new start-ups per year from 2016 to 2019).

[1] Several studies analyse the issue from different perspectives and metrics and find overall lower performance for Chinese patents, e.g., large citation lag (which indicates lower value of the patent), large shares of domestic citations and of self-citations, alternate effects (depending on the sector) in terms of consequences on firms' productivity, less accurate or shorter description of the innovation, and few number of claims that Chinese patents on average contain (Fisch et al., 2017; Christodoulou et al., 2018; Boeing at al., 2019, Song, 2014).